Introduction

CoStar Group, a leading provider of real estate information services, has announced its intention to acquire Matterport, the virtual tour platform, for an enterprise value of $1.6 billion. Although promising, this acquisition is subject to regulatory and shareholder approval, thus creating an interesting arbitrage opportunity for investors.

Details of the Acquisition

In April, CoStar announced that each Matterport shareholder will receive $2.75 in cash and $2.75 in CoStar shares. However, the stock portion is subject to a “symmetrical collar” mechanism, which can influence the final value of the distributed shares.

Collar Mechanism

The average price of CoStar shares will be determined three days before the acquisition, based on the volume-weighted average price over the previous 20 consecutive trading days. If the average price of CoStar shares is between $77.42 and $94.62, the exchange ratio will be calculated by dividing $2.75 by the average price. If the price is below $77.42, the exchange ratio will be 0.03552, and if it is above $94.62, it will be 0.02906.

Arbitrage Opportunity

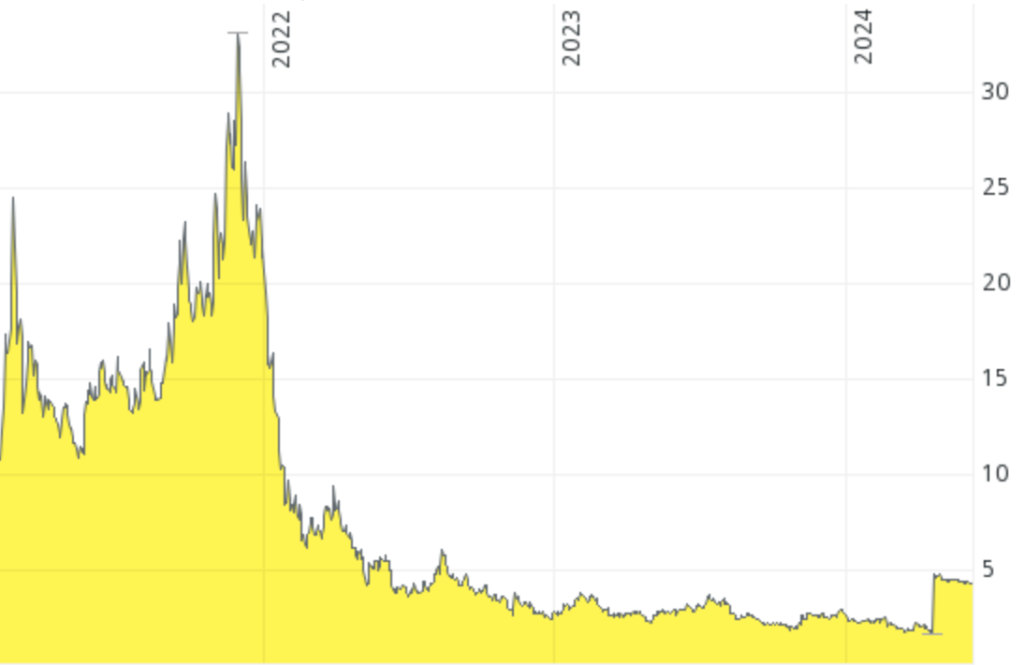

Currently, Matterport shares are traded at approximately $4.26 (as of June 6, 2024), while CoStar shares are at $77.05, creating a margin of about 22% (5.487 USD vs. 4.26 USD) between the trading price and the expected purchase price. This difference represents an arbitrage opportunity for investors.

Considerations for Arbitrage

To evaluate the arbitrage opportunity, it is important to answer four key questions:

- How likely is it that the promised event will occur?

- The merger must be approved by Matterport shareholders and regulatory authorities. Matterport management, which owns about 15% of the shares, has already voted in favor of the agreement, making shareholder approval likely. However, regulatory approval remains an uncertainty, especially in a context where antitrust authorities are increasing their scrutiny of mergers and acquisitions.

- How long will the money be tied up?

- CoStar and Matterport management expect the agreement to be concluded by the end of 2024. If this happens, a 22% return in about seven months is particularly attractive, considering that six-month US Treasury bills currently yield about 5.4%.

- What is the probability of a better offer emerging?

- Since the agreement was announced in April and no other offers have emerged, it seems unlikely that a competing offer will surface.

- What happens if the event does not occur?

- If the acquisition fails, Matterport will receive a termination fee of $85 million from CoStar. Matterport, while not yet profitable, has shown steady growth in its subscriber base and has a solid balance sheet with $419 million in cash and investments. However, Matterport shares were trading at $1.74 before the offer, indicating significant downside risk.

Evaluation of Matterport as an Independent Company

In the first quarter of 2024, Matterport generated $39.9 million in revenue, a year-over-year increase of 5%. Although the growth is disappointing, the company surpassed one million subscribers, with a 30% increase compared to the previous year. Its dependence on the real estate sector, currently struggling due to high interest rates, poses a challenge. However, the strong cash position and debt-free status make Matterport an interesting company even as an independent entity.

Regulatory Risks

One of the main risks associated with this acquisition concerns antitrust approval. CoStar has faced regulatory scrutiny in the past, as in the case of its acquisition of RentPath, which was blocked by the Federal Trade Commission (FTC) in 2020. However, the acquisition of Matterport represents a vertical integration rather than a horizontal one, which could alleviate regulatory concerns.

Currently, there have been no significant updates regarding the HSR (Hart-Scott-Rodino Antitrust Improvements Act) review, but the fact that there have been no extensions of the review period suggests that antitrust issues may not be insurmountable.

We have asked CoStar’s IR department for confirmation regarding the 30-day HSR review period, which would have expired on June 3, twice without receiving a response. According to informed sources, there has been a refiling (which allows additional information to be added without incurring additional costs), and the 30-day period has restarted. Specialized funds in these opportunities – at least those we follow – have so far only taken relatively small positions, indicating that specialists remain very cautious, likely due to antitrust risks.

Final Considerations

The arbitrage opportunity presented by the acquisition of Matterport by CoStar is interesting for investors willing to take on a short-term risk. The likelihood that the agreement will overcome regulatory hurdles seems slightly favorable (although with the Biden administration, there is always an antitrust risk!) and the margin of 22% is attractive. However, it is essential to closely monitor the decisions of the Federal Trade Commission and the Department of Justice, as well as significant fluctuations in CoStar’s share price.

For investors who believe in the recovery of the real estate market, Matterport could also be a valid option as an independent company. With a strong subscriber base and a solid financial position, the company has the potential to grow despite the current challenges in the sector.

This investment is currently only interesting for specialists because the risk is asymmetrically unfavorable (high downside, 22% upside) even though the 22% upside seems attractive. Therefore, I would wait for further confirmations regarding antitrust approval before proceeding in a big way.